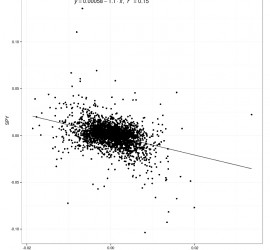

Linear model for two asset return series

First we’ll get the prices of two ETFs, one is the S&P 500 tracker (SPY) and the other is the US 7-10y Treasury ETF (IEF). For the purpose of regression we will convert into log returns: Now the linear regression where we model the daily S&P 500 returns using the […]