library(zoo)

library(ggplot2)

getshiller <- function(source="http://www.econ.yale.edu/~shiller/data/ie_data.xls",cachefile="shiller.RData") {

library(gdata)

if (file.exists(cachefile)) {

load(cachefile)

return(x)

}

xraw <- read.xls(source, sheet = 1, verbose=FALSE, perl="perl")

xraw[xraw=="#N/A"] <- NA

rawrows <- dim(xraw)[1]

rawcols <- 11

t.x <- as.Date(sprintf("%4.2f.01",as.numeric(as.vector(xraw[,1]))),"%Y.%m.%d")

ok <- !is.na(t.x)

x <- zoo(as.numeric(as.vector(xraw[ok,2])),t.x[ok])

for ( i in seq(3,rawcols) ) {

z <- zoo(as.numeric(as.vector(xraw[ok,i])),t.x[ok])

x <- merge.zoo(x,z)

}

colnames(x) <- c("P","D","E","CPI","DateFraction","LongRate","P.real","D.real","E.real","CAPE")

save(x,file=cachefile)

return(x)

}

shiller <- getshiller()

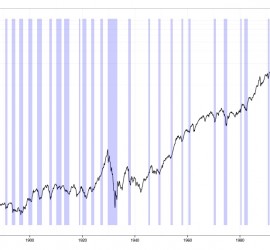

ggplot(fortify(shiller[,c("P.real","CAPE","LongRate")],melt=TRUE)) +

geom_line(aes(x=Index,y=Value,colour=Series)) +

facet_grid(Series ~ .,scales = "free_y") +

theme_bw() +

theme(legend.position="none",axis.title.x=element_blank(),axis.title.y=element_blank())